Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Protect Your Pipes

Depending on the region of the United States you’re in, you’ll need to protect your pipes from bursting this winter.

According to statistics, it seems so. However, like many things, there’s an art to it. When depersonalizing your home, it’s crucial to find a balance between making it less personal and not stripping away its warmth and humanity. The aim is to present your home as clean, inviting, and cozy, allowing potential buyers to envision a happy life in it. To achieve this, it’s recommended to declutter, organize, clean, and stage your home before listing photos are taken. Read a more in depth description of the secret to selling your home quickly below.

While you may have grown accustomed to the lived in odors and oddities of your home, potential buyers may notice dust bunnies, kitchen grease, and mysterious stains. To avoid giving them a negative impression, take the time to deep clean your home before showcasing it.

If you’re considering a move, decluttering should be a priority. It not only reduces the items you’ll need to transport but also creates a sense of openness, making your home appear larger. A decluttered home allows architectural features to shine and suggests that the property has been well-maintained.

Humans naturally find comfort in organized spaces. It provides a sense of understanding, safety, and control. To read more about this theory I recommend you read this article. Organization can be a key selling point during an open house. Additionally, an organized home looks appealing in listing photos, which are crucial for attracting potential buyers.

Staging is essential to help buyers connect with the stories your home tells. While you can hire a professional, you can also stage your home yourself by following the first three steps. Simplify spaces, give each area a clear purpose, and clean. Consider the market climate; in a seller’s market, you might not need extensive efforts to attract attention, but thoughtful staging can still lead to a bidding war and higher payouts.

Your realtor will work with you to make additional recommendations based on the current market conditions. Overall, this proven method can fast-track you to a successful and timely sale.

With fluctuating interest rates and market volatility, it’s not uncommon for potential buyers and sellers to feel a bit apprehensive about making a move right now. It’s like playing a game where the rules can change at any moment. But what if I told you that there’s a way to navigate this game successfully and conquer your Real Estate fears?

The fear of the unknown is one of the most common reasons people hesitate when it comes to buying or selling real estate. The constant shift in interest rates and unpredictable market trends can indeed be scary. However, understanding these fears and knowing how to manage them is the first step towards success.

Is it the fear of making a wrong decision, or perhaps the fear of losing money? Or maybe it’s the fear of not being able to keep up with the fast-paced nature of the real estate market? Or losing your 3% mortgage rate? Whatever your fear may be, acknowledging it is the first step towards overcoming it.

This is where Windermere Mill Creek comes in. With decades of experience and a deep understanding of the real estate market, especially in Snohomish County, we can provide the guidance and advice you need to ease your mind.

The real estate market, like any other market, will always have its ups and downs. Interest rates will fluctuate, and market trends will change. But with the right guidance, knowledge, and a bit of courage, you can navigate any market successfully.

Continued Education. Yep, it’s that simple. We stay plugged in here at Windermere Mill Creek. Our education program is ongoing because the pursuit of knowledge is a limitless journey. As a result, we offer comprehensive weekly training programs, two monthly office meetings which often feature guest speakers in the field, and many other opportunities for our Agents to intermingle with the goal of learning to best service our clientele. That way, when the market shifts, we keep moving right along with it.

If you’re ready to take the plunge and dive into the real estate market in Washington State, we’re here to help. We’ll provide you with the tools, resources, and expertise you need to navigate this complex landscape. So, are you ready to play the real estate game? Because we’re ready to help you win!

425-481-6666

millcreek@windermere.com

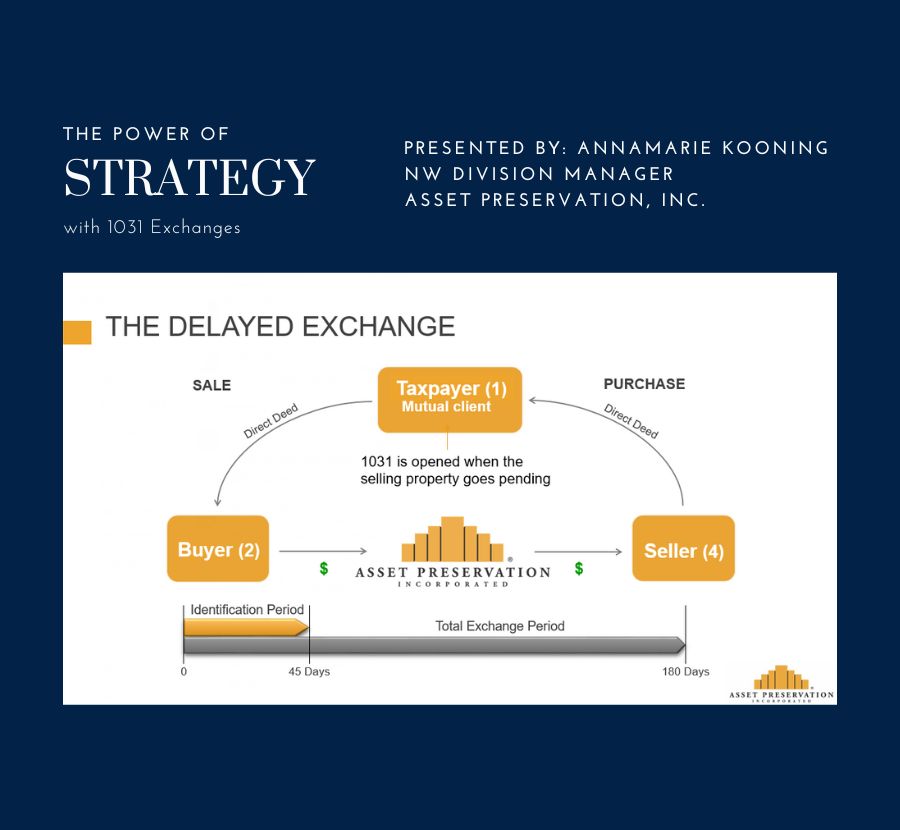

We recently had the pleasure of hosting a seminar on wealth preservation led by Annamarie Kooning, the NW division manager of 1031-Asset Preservation Inc. The topic was especially relevant in that we have experienced unparalleled real estate appreciation for the last decade, with the drawback being the tax implications when selling a long held real estate asset.

Credit: ANNAMARIE KOONING | NW Division Manager | Asset Preservation, Inc. | The Power of Strategy with 1031 Exchanges

A 1031 tax deferred exchange is a powerful tax strategy that allows real estate investors to defer paying capital gains taxes on the sale of an investment property, provided they meet certain IRS requirements.

1. Tax Deferral: The biggest benefit of a 1031 exchange is the tax deferral. By exchanging a property instead of selling it, an investor can defer paying capital gains taxes on the sale, potentially indefinitely. This allows the investor to keep more of their proceeds working for them, and to defer paying taxes until a later date.

2. Increased Buying Power: Another advantage of a 1031 exchange is that it allows investors to use the equity in their property to purchase a more valuable property, without having to pay taxes on the sale of the first property. This can increase the investor’s buying power and enable them to purchase a property that may generate more income or appreciate more quickly.

3. Diversification: A 1031 exchange also allows investors to diversify their real estate holdings. By exchanging one property for another, an investor can adjust their portfolio to better meet their investment goals, such as increasing cash flow, reducing risk, or capitalizing on emerging trends.

4. Estate Planning: Finally, a 1031 exchange can also be a useful tool for estate planning. By deferring taxes on a property, an investor can pass it on to their heirs without having to pay capital gains taxes. This can help to preserve the investor’s wealth for future generations.

Overall, a 1031 exchange can be a powerful tax strategy for real estate investors, allowing them to defer taxes, increase buying power, diversify their holdings, and plan for the future.

Contact us for more information, or for an introduction to our 1031 tax code expert, Annamarie Kooning. It may save you thousands of dollars.

We all look forward to vacations for months, and it’s maybe the only opportunity to enjoy a few consecutive stress-free days away from the typical day-to-day pressures of work and life. You’ll want to make sure that while you’re away, your home is safe and secure.

The most obvious option is to invest in some high-end home security devices; however, those can be very pricy, and wouldn’t you rather put that money toward your getaway instead? If so, we’ve got you covered with five tips that you can use to increase the security of your home while you’re on your next vacation.

Having lights on in your home is one of the most obvious indicators that the home is not empty. However, if you’re planning to go away for several days, or several weeks at a time, keeping the lights on for the entire duration of your trip is not only going to drive your electric bill through the roof, but it’s also dangerous as it poses a risk for fires.

Light timers are a great and cost-effective way to increase the security of your home while you’re away. You can set the timers to automatically turn your lights on and off at the same times that they typically would be if you were home. You can set up a few throughout the different floors of your home so it appears that people are around and occupying both the upstairs and downstairs.

If you’re going to be away for more than a day or so, a smart idea is to have a trusted friend or neighbor come by to check up on your home a couple of times. Not only will this help to ensure that everything is right within your home, but it will also bring some motion and human presence to your house.

Unless you have to use your car to get to your vacation destination, leaving it parked in the driveway can be a a great option for increasing your home’s security while you’re not there. It’s all about creating the illusion that someone is home, even when that’s not the case. Although you might be planning to use your car to drive to where you’re going. If that’s the case, a good alternative is to ask a nearby friend or neighbor if they would be willing to park their car in your driveway while you’re away. To sweeten the deal, offer to pay for their next carwash when you get back.

If you typically keep your blinds closed throughout the day, keep them closed while you’re away. However, if it’s more common for you to leave them open for the majority of the day, mimic this while you’re gone, and make the choice to keep them open. The recurring theme here is doing little things in order to generate the impression that you’re still home, so consider leaving your curtains and blinds in a position that is more like how they are on a normal daily basis.

By putting up decoy security signs, stickers and even imitation cameras in plain sight, you’re increasing your chances of deterring trespassers from trying to enter your home or approach your property. If it looks like a security system is installed, and it’s not hidden, it’s unlikely that someone would try to break in if they saw it.

While we don’t recommend this as your only means of protecting your home but by putting up decoy security signs, stickers and even imitation cameras in plain sight, you’re increasing your chances of deterring trespassers. If it looks like a security system is installed, and it’s not hidden, it’s unlikely that someone would try to break in if they saw it. This should help to give you the peace of mind that you need in order to enjoy your vacation and know that your home will be adequately safe and secure until you return back.

blog post by Chasity Rodriguez

Social Media Director

No matter how many HGTV shows you watch about flipping old houses that have happy endings, reality isn’t always as kind. Regardless of when the home was built and its current condition, if you find yourself in a situation where you’re getting ready to make an offer, ask yourself these questions first to make sure it really is the right house for you (and your budget).

Here are some questions to consider to help you determine whether this is your best option:

As heartbreaking as it may be to walk away from what you think could be your dream home, the reality is, it might not work out. And it’s better to know that now, than after the papers are signed.

Here is Part two of Moving and Packing Tips. Pack a “first day” box with items you will need right away (dogs and cats included, hahaha….)

scissors

utility knife

local phone book

coffee cups

teakettle

instant coffee or tea, soft drinks

pencil and paper

soap

bath towels

trash bags

shelf liner

paper plates

snacks

toilet paper

children’s toys and books

furniture pads

hand truck or dolly

packing tape

bubble wrap

newspapers or

packing paper

scissors

utility knife

labels

felt-tip markers

cornstarch packing

“peanuts”

plenty of boxes

Pick up the truck as early as possible if you are

moving yourself.

Make a list of every item and box loaded on the truck.

Let the mover know how to reach you.

Double-check closets, cupboards, attic, basement

and garage for any left-behind items.

Be on hand at the new home to answer questions

and give instructions to the mover.

Check off boxes and items as they come off the truck.

Install new locks. Confirm that the utilities have been turned on and

are ready for use.

Unpack your “first day” box (see list above for suggested

contents).

Unpack children’s toys and find a safe place for them to play.

Examine your goods for damage.

written by Chasity Rodriguez

Social Media Director

The process of moving is long and complex. Being organized, knowing what needs to be done,

and tackling tasks efficiently can make your move significantly less stressful. We have some moving and packing tips for you and a detailed list to keep you on task and help make your move successful.

Use up things that may be difficult

to move, such as frozen food.

Get estimates from

professional movers or from

truck rental companies if you

are moving yourself.

Once you’ve selected a mover,

discuss insurance, packing,

loading and delivery, and the

claims procedure.

Sort through your possessions.

Decide what you want to keep,

what you want to sell and what

you wish to donate to charity.

Record serial numbers on

electronic equipment, take photos

(or video) of all your belongings

and create an inventory list.

Change your utilities, including

phone, power and water, from your

old address to your new address.

Obtain a change of address

packet from the post office

and send to creditors,

magazine subscription offices

and catalog vendors.

Discuss tax-deductible moving

expenses with your accountant

and begin keeping accurate

records.

If you’re moving to a new

community, contact the

Chamber of Commerce and

school district and request

information about services.

Make reservations with airlines,

hotels and car rental agencies,

if needed.

If you are moving yourself, use

your inventory list to determine

how many boxes you will need.

Begin packing nonessential items.

Arrange for storage, if needed.

If you have items you don’t want to

pack and move, hold a yard sale.

Get car license, registration and

insurance in order.

Transfer your bank accounts to

new branch locations. Cancel

any direct deposit or automatic

payments from your accounts if

changing banks.

Make special arrangements to

move pets, and consult your

veterinarian about ways to make

travel comfortable for them.

Have your car checked and

serviced for the trip.

Collect items from safe-deposit

box if changing banks.

Defrost your refrigerator

and freezer.

Have movers pack your

belongings.

Label each box with the contents

and the room where you want it

to be delivered.

Arrange to have payment ready

for the moving company.

Set aside legal documents

and valuables that you do not

want packed.

Pack clothing and toiletries,

along with extra clothes in

case the moving company

is delayed.

Give your travel itinerary to a close

friend or relative so they can reach

you as needed.

written by Chasity Rodriguez

Social Media Director

by Chasity Rodriguez

It’s the New Year, but you’re probably back to your same old work from home schedule—taking calls from your couch, working late hours, and even checking emails on the weekends. In the midst of this ongoing pandemic, our work life has merged with our personal life so that there’s little separation between the two. “Many employers are piling greater responsibilities on their staff and promoting a culture of open communication outside of traditional work hours. Due to fear of losing their jobs, many individuals working from home feel obligated to meet these demands,” says Jeffrey Ditzell, D.O., a psychiatrist based in New York City. When work and life are under the same roof, it can be difficult to keep them balanced.

As hard as it may be in these times, maintaining a healthy balance between your work and your personal life is essential for your mental and physical health. People who have blurred, or nonresistant, boundaries between their work and personal lives tend to have higher levels of stress and feel more distressed over time. Eventually developing all of the health issues that come along with it, but the good news is you can prevent this imbalance and all of the negative impacts of it by drawing a fine line between your personal and professional life.

“Setting firm boundaries is crucial for a strong work-life balance,” says Regine Muradian, Psy.D., a clinical psychologist based in Los Angeles. Learning how to establish boundaries will set you on the route to keep your work-related activities in control and prioritize more time for yourself, even when the pandemic is over. Here are five Tips for a Healthy Work-Life Balance that will help you build great WFH habits.

Designate when you will start and end the workday. When you set these times in stone (as best as you can), avoid checking your work email or accounts outside of your allotted work hours. Use technology to your advantage by using the various apps and digital reminders that make it more difficult for you to break your own rules and access things outside of work time. Although technology can feel like it’s taking over our lives and infringing on our work-life balance, we can actually use it to our benefit in helping us stick to the boundaries we know are healthy for us. This can mean setting time limits, turning off your active status, or even activating an auto-reply to let others know you’re not available outside your work hours.

An imbalance between your work and personal life can be emotionally draining and cause burnout. Ensure you’re getting enough time each day to decompress and rest, which is necessary for your health and well-being. Make a habit to incorporate at least 10 minutes of mindfulness or yoga in your day. Prioritizing this time will help you check in with yourself in regards to how you’re feeling. To boost your mood and start the day with an energy boost, incorporate physical activity in your routine too. Pick any workout you enjoy and perform it regularly. This will enhance your mood and improve your experience of your day. Whether it is the first thing in the morning, during lunchtime, or before bed, creating time and space for consistent exercise and mindfulness will help you feel relaxed and rejuvenated.

Set aside time regularly to do the things you love with those you love. Plan special dates that you’ll look forward to and don’t overlap with your work hours. This may include attending an online workout class, having a Zoom happy hour with friends, taking a walk with your partner, or anything else you want to make sure you fit into your day or week. You can also invest in more family time by checking in with your loved ones virtually and attending events, like birthdays and anniversaries. If you have any family events that may occur on a consistent basis, build your work schedule around those events instead of building those events around your work schedule, if possible.

The COVID-19 pandemic is the perfect time to reflect on your interests and adopt a new hobby that you love. If you’re WFH, you’re probably saving a lot of time and money on commuting, so why not put it toward a new activity or skill? Maybe it’s joining that 8 a.m. running club in your neighborhood, or growing flowers in your home garden, or perhaps learning a new language. Think about something that feels good to you and will help you decompress. This may be a good time to avoid the news, social media and just do something for yourself. Finding purpose in a hobby will not only spark your inner creativity but also uplift and motivate you.

While there may not be much to do on a vacation during a pandemic, you still need that time off for your mental health and well-being. Do something that comforts you—maybe it’s taking a staycation and doing a movie marathon or spending a week in your favorite city. During your vacation, make sure to mute all work-related emails and accounts, if possible, and just focus on having fun. Additionally, throughout the year, don’t be too hard on yourself—take breaks every so often for that much-needed “me time.” Reflect and evaluate when you need time off from work, which will shift you closer to the type of balance you are striving for. It is a process for most people, so reviewing and tweaking your schedule, habits, and boundaries regularly is important.

By Chasity Rodriguez

Social Media Director

IN A TIME DEFINED IN many ways by the coronavirus pandemic, everyday life is affected constantly as we adapt to changing circumstances. One of the many effects of the pandemic is that more and more people are buying or adopting pets, sometimes referred to as “pandemic puppies,” than ever before.

Simultaneously, an increasing number of people are sheltering in place or being uprooted and going through multiple moves due to major life shifts in how they work or go to school. For many families, that means packing up and making a move with their furry friends in tow.

Moving is not necessarily a fun activity, and we often don’t take into consideration just how stressful it can be for our four-legged friends. Animals, like people, need time to adjust. But with smart preparation and planning, you can make the move successful and easier for your pet, for you and for your new home.

Here are five tips to make moving with your pet as pleasant and stress-free as possible:

Introduce your pet to your new home and surroundings the way you might introduce young children to the space (they’re called “fur babies” for a reason, after all). Most people bring their children to their new home a few times prior to an actual move to get them excited about the house and neighborhood. This gives them time to explore and visualize themselves in the new environment and can alleviate some of the stress that may carry over with the major transition.

Try this with your dogs, too – let them sniff around while you’re taking measurements for furniture. Take them for a walk around the block so they can start to familiarize themselves with their new surroundings. Seek out any local dog-friendly parks and research where the best veterinarians and doggy day cares are. You’ll both come to rely on these resources, and it’ll be a great way to meet new people in your neighborhood.

You may be tempted to throw away old, worn-out items prior to your move, but you’ll be glad that you didn’t get rid of your dog’s favorite chew toy or your cat’s beloved scratching post. Having these familiar items present in their new spaces will be key to helping them acclimate and feel right at home.

If you really hate that old dog bed, it doesn’t have to stay in your new house long-term. Keep it around for the first few weeks until the dog adjusts and feels comfortable in its new space. Think about how you would feel if someone tossed your favorite pillow that you simply cannot sleep without.

The same goes for cats. You may feel inclined to get a brand-new litter box for your new home, but hang onto the one they’re familiar with while they get used to the new setting.

No one enjoys the mayhem of moving day. The house is a mess, movers are rummaging around and you’re scrambling to do your best to make sure it all goes as smoothly as possible.

It may be a smart move for families with children to send them to stay with a family member or friend on the actual move day, and do the same with your pet, if possible. You don’t want them to associate their new home with the inevitable chaos and the frazzled mood you are sure to feel on moving day. If you don’t have someone that lives nearby, drop them off at day care or ask a new neighbor if they’d be willing to help.

A move can make pets act abnormally – your dog may decide to use the floor as a bathroom or a cat may scratch up the carpeting. To avoid these potentially costly damages, try to protect your new home as if you were dealing with a new puppy or kitten with some simple precautions.

Lay floor mats down or cover the couch temporarily until you know all the moving jitters have subsided. An accident can create more stress for both of you, and tarnish what should be a loving and peaceful new environment.

Cats, in particular, are more likely to feel anxious about their new surroundings. A way to ease their anxiety is to limit their initial access to the whole house or apartment. Create a home base for them in one room that has their favorite toys, water, treats and a litter box, and allow them to acclimate on their own time. Once they’re comfortable there, you can open up additional space for them to explore room by room. If your cat’s home base isn’t the final destination for its litter box, slowly move it closer to the permanent location each day.

Finally, don’t forget to change your pet’s address tags when you relocate. With time, patience and smart planning, everyone will start off on the right foot (or paw) in your new home.

Chasity Rodriguez

Social Media Director

Windermere Mill Creek

by Chasity Rodriguez

Make sure your home is safeguarded against subfreezing temperatures. Our checklist will help you ensure you’re prepared.

Depending on the region of the United States you’re in, you’ll need to protect your pipes from bursting this winter.

Weather stripping or installing storm doors and windows will prevent cold air from entering your home or heat from escaping it, which will reduce your power bills. Door sweeps are also an effective and easy way to keep the cold out.

Animal nests or creosote buildup in your fireplace can be hazardous. Have an annual inspection before building your first fire of the season. Also, soot and other debris build up in the chimney. Call a chimney sweep to thoroughly clean the chimney before your first winter use. You should also vacuum or sweep out any accumulated ash from the firebox.

Cleaning your gutters is an important part of winter prep. A good rule of thumb is to have the gutters cleaned as soon as the last leaves have fallen in the autumn. To prevent clogging, inspect and clean the gutters of leaves and other debris. Clean gutters will also allow melting snow to drain properly.

If you want to avoid gutter cleanings, consider gutter guards. They can be made of stainless steel or polyvinyl chloride (PVC) and will help keep out leaves, pine needles, roof sand grit and other debris from your gutter. They need to be occasionally brushed off to ensure the guards work to their maximum effectiveness, but it’s not as strenuous as routine cleanings.

Caulk around windows and use foam outlet protectors to prevent cold air from entering your home. However, the majority of heat loss typically occurs via openings in the attic. Check to make sure that you have enough insulation.

In the winter, the Department of Energy suggests keeping the thermostat at 68 degrees Fahrenheit when you’re at home. Lower the thermostat a few degrees while you’re away or sleeping. Switching your thermostat out for a programmable version is a good idea. It’ll let you customize your heating so the system doesn’t run when you don’t need it, keeping your home comfortable and bills down.

Install a Programmable Thermostat

You’ll need to bring plants and flowering trees inside before the first cold snap. Typically, you should bring your plants in before temperatures dip below 45 degrees Fahrenheit.

Cold temperatures, snow and ice can damage outdoor furniture and grills. If possible, store them in the garage or basement. If you have a gas grill with a propane tank, close the tank valve and disconnect the tank first. It must be stored outside. If you don’t have storage space for your items, purchase covers to protect them from the elements. You also need to maintain your grill and cover it before putting it away for the season.

Outdoor power tools, such as mowers and string trimmers, need to be cleaned and maintained prior to storing. If you have a snow blower, it’s time to inspect it before the first snowfall to ensure it’s working properly.

Call your local power company to see if they conduct energy saving assessments. It’s often a free service where a representative will identify specific changes to make your home more energy efficient and save you money. In addition to the suggestions above, LED light bulbs and water heater blankets can also make a difference.

Your furnace will function more efficiently with a clean filter. A dirty filter with trapped lint, pollen, dust, etc., obstructs airflow and makes your furnace run longer to heat your home. Replace filters at least every three months.

Snow, rain, ice and wind can make it challenging for your home to withstand winter’s wrath. Of particular concern should be your roof. You can get a head start on winterizing your roof with a few key steps.

To help keep chilly air from leaking in through window cracks, swap out the lightweight summer curtains with thermal lined curtains or drapes. They’ll help keep your home warm and lower your heating bill. For the windows that don’t get direct sunlight, keep the curtains or drapes closed to keep the cold air out and the warm air in.

Don’t wait for the next big winter storm. Depending on where you live, there are certain staples that are good to stock up on ahead of time.

Written by Chasity Rodriguez

Social Media Director

© 2026 Windermere Real Estate